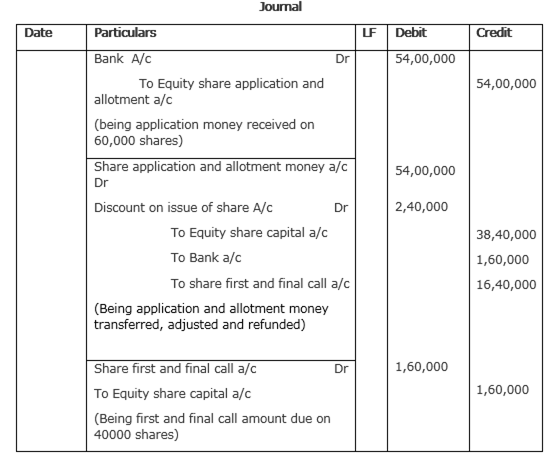

XYZ Ltd. invited applications for 40,000 equity shares of Rs 100 each at a discount of 6%. The amount was payable as follows:

On Application and Allotment Rs 90 per share. On First and Final call the balance amount. Application for 60,000 shares were received. Applications for 10,000 shares were rejected and shares were allotted on pro-rata basis to remaining applicants. Excess application money received on application and allotment was adjusted towards sums due on first and final call. The calls were made. A shareholder, who applied for 50 share, failed to pay the first and final call money. His shares were forfeited. All the forfeited shares were re-issued at Rs 97 per share fully paid up.

Pass necessary journal entries for the above transactions in the books of XYZ Ltd.

Important Note: As the shareholder has already paid excess amount than required on first and final call as he has applied for, this answer cannot proceed further.

Calculation of excess amount received

Amount received = 50*90=4500

Less amount to be received = 40*90=3600

Excess amount received= 900 Rs

Amount due on first and final call = 40*4 = Rs 160.

As he has already paid amount of Rs 900 in excess at the time of application and allotment, forfeiture is not possible in this case.

Thus, this question has incomplete or wrong information, hence, cannot be solved fully.

Calculation of total amount to be refunded.

Amount paid by 50,000 shares = 45, 00, 000

Less amount to be paid = 36, 00, 000

Excess application money received = 9,00,000

Less amount due on first and final call = 1, 60,000

Amount refunded through bank = 7,40,000

Add amount to be refunded = 9,00,000

Total =16,40,000

What rate of interest the company pays on calls - in advance if, it has not prepared its own Articles of Association?

If a company has not prepared its own Article of Association, then it has to pay interest on Calls-in-Advance at a rate not exceeding 6% which is prescribed in the Table A of the Companies Act of 1956.

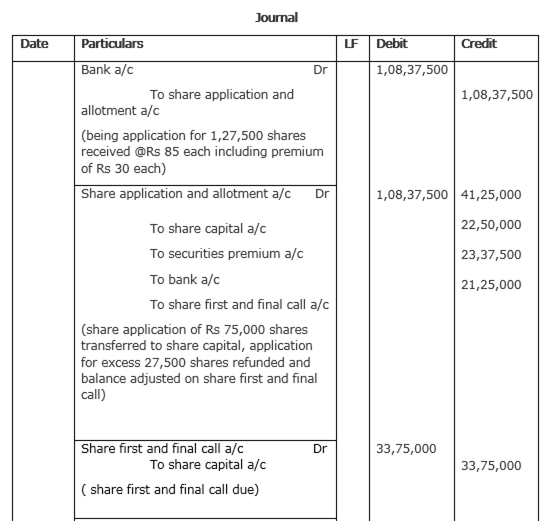

AB Ltd. invited applications for issuing 75,000 equity shares of Rs 100 each at a premium of Rs 30 per share. The amount way payable as follows:

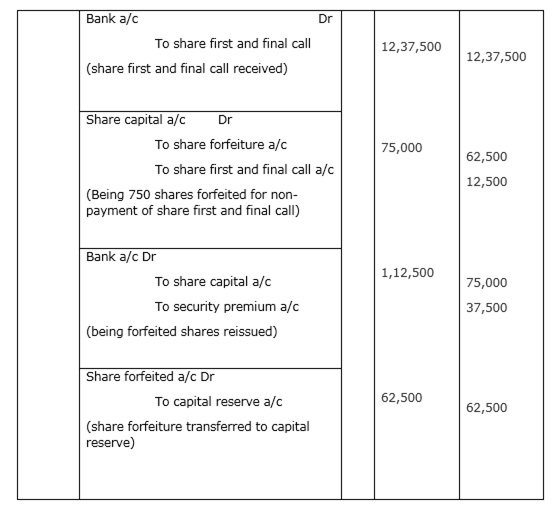

On Application and Allotment Rs 85 per share (including premium)On First and Final call the balance Amount Applications for 1,27,500 shares were received. Applications for 27,500 shares were rejected and share were allotted on pro-rata basis to the remaining applicants. Excess money received on application and allotment was adjusted towards sums due to first and final call. The calls were made. A shareholder, who applied for 1,000 shares, failed to pay the first and final call money. His shares were forfeited. All the forfeited shares were reissued at Rs 150 per share fully paid up.

Pass necessary journal entries for the above transactions in the books of AB Ltd.

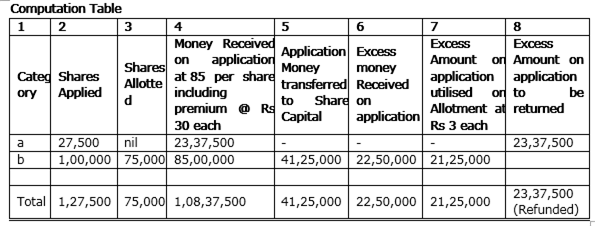

Those who applied for 100000 shares are allotted 75,000 shares

Those who applied for 1000 shares are allotted 75,000*1,000/1,00,000 =750 shares

Shares application and allotment received on 1,000 shares of Rs 85 each = Rs 85,000

Shares allotted = 750*85 = 63,750 Rs

Excess application and allotment money received = Rs 21,250

Share first and final call due on 750 shares of Rs 45 each = Rs 33,750

Excess application and allotment money received = 21,250 Rs

Share first and final call not received = Rs 12,500 ( 33,750-21,250)

Therefore share first and final call received = 12,37,500 (12,50,000-12,500)

What is meant by Securities Premium?

When shares are issued at an amount more than the nominal value or par value, it is called shares issued at premium. The premium amount thus received is credited to a separate account called ‘Securities Premium Account’ and is shown on the liabilities side of the company’s balance sheet under the head ‘Reserves and Surpluses’.

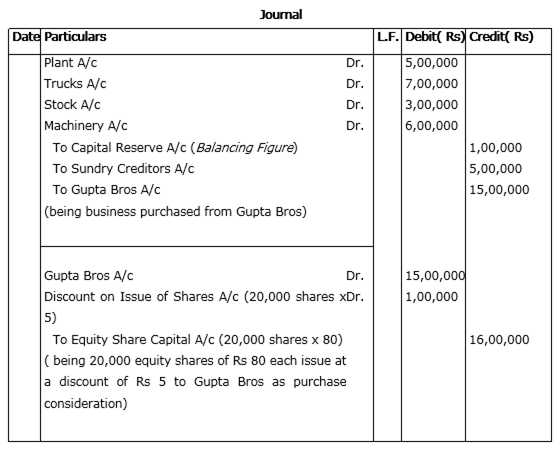

Madhav Ltd. issued fully paid equity shares of Rs. 80 each at a discount of Rs. 5 per share for the purchase of a running business from Gupta Bros. for a sum of Rs. 15,00,000.

The assets and liabilities consisted of the following:

Plant Rs. 5,00,000; Trucks Rs. 7,00,000; Stock Rs. 3,00,000; Machinery Rs. 6,00,000 and Sundry Creditors Rs. 5,00,000.

You are required to pass necessary journal entries for the above transactions in the books of Madhav Ltd.

Working Note:

Calculation of Number of Equity Shares Issued:

Purchase consideration = 15,00,000

Number of equity shares to be issued = 15,00,000/(80-5)

=15,00,000/75 = 20,000 equity shares

Switch

Switch