Giving reasons, state whether the following statements are true or false.

A monopolist can sell any quantity he likes at a price.

False, a monopolist cannot sell any quantity he likes at a price because the monopolist controls only the supply and not the demand. A monopolist can only determine one of two things. It has to be either price or quantity; this is because there is a fixed price consumers are willing to pay for a given quantity. As a result a monopolist can only charge the price corresponding to the specific quantity he has set otherwise the goods he has produced won’t be sold. This is because he has no control over the quantity that he can sell in the market. Rather, it depends on the buyers that what quantity of output they want to purchase at the price fixed by the monopolist. If the monopolist fixes a higher price, then lesser quantity of the output will be demanded and lesser quantity will be sold in the market. On the other hand, if he fixes a lower price, then higher quantity of the good will be sold.

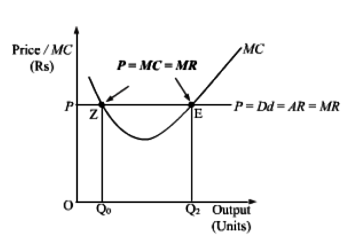

Why is the equality between marginal cost and marginal revenue necessary for a firm to be in equilibrium? Is it sufficient to ensure equilibrium? Explain.

Equilibrium refers to a state of rest when no change is required. A firm (producer) is said to be in equilibrium when it has no inclination to expand or to contract its output. This state either reflects maximum profits or minimum losses.

According to MC=MR approach, As long as MC is less than MR, it is profitable for the producer to go on producing more because it adds to its profits. He stops producing more only when MC becomes equal to MR.

When MC is greater than MR after equilibrium, it means producing more will lead to decline

in profits.

Both the conditions are needed for Firm’s Equilibrium:

1. MC = MR:

MR is the addition to TR from sale of one more unit of output and MC is addition to TC for

increasing production by one unit. Every producer aims to maximize the total profits. For

this, a firm compares it’s MR with its MC. Profits will increase as long as MR exceeds MC

and profits will fall if MR is less than MC. So, equilibrium is not achieved when MC < MR

as it is possible to add to profits by producing more. Producer is also not in equilibrium

when MC > MR because benefit is less than the cost. It means, the firm will be at

equilibrium when MC = MR.

2. MC is greater than MR after MC = MR output level:

MC = MR is a necessary condition, but not sufficient enough to ensure equilibrium. Only

that output level is the equilibrium output when MC becomes greater than MR after the

equilibrium.

It is because if MC is greater than MR, then producing beyond MC = MR output will reduce

profits. On the other hand, if MC is less than MR beyond MC = MR output, it is possible to

add to profits by producing more. So, first condition must be supplemented with the

second condition to attain the producer’s equilibrium.

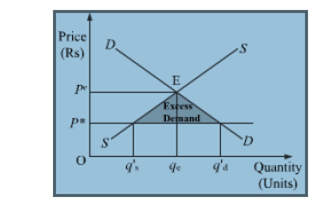

Explain the effects of 'maximum price ceiling' on the market of a good'? Use diagram.

A price ceiling is a government-imposed price control or limit on how high a price is charged for a product. Governments intend price ceilings to protect consumers from conditions that could make necessary commodities unattainable. It is the legislated or government imposed maximum level of price that can be charged by the seller. Since price ceiling is lower than the equilibrium price thus the imposition of the price ceiling leads to excess demand as shown in the diagram below.

The following are the consequences and effects of price ceiling:

1) An effective price ceiling will lower the price of a good, which decreases the producer surplus. The effective price ceiling will also decrease the price for consumers,but any benefit gained from that will be minimized by the decreased sales due to the drop in supply caused by the lower price.

2) If a ceiling is to be imposed for a long period of time, a government may need to ration the good to ensure availability for the greatest number of consumers.

3) Prolonged shortages caused by price ceilings can create black markets for that good.

4) Due to artificially lowering the price, the demand becomes comparatively higher than the supply. This leads to the emergence of the problem of excess demand.

5) The imposition of the price ceiling ensures the access of the necessity goods within the reach of the poor people. This safeguards and enhances the welfare of the poor and vulnerable sections of the society.

6) Each consumer gets a fixed quantity of good (as per the quota). The quantity often falls short of meeting the individual’s requirements. This further leads to the problem of shortage and the consumer remains unsatisfied.

7) Often it has been found that the goods that are available at the ration shops are usually inferior goods and are adulterated and infiltrated.

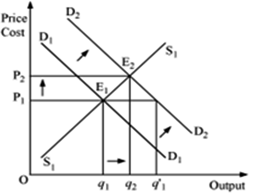

Market for a good is in equilibrium. The demand for the good 'increases'. Explain the chain of effects of this change.

Equilibrium is defined as a situation where the plans of all consumers and firms in the market match and the market clears. When the supply and demand curves intersect, the market is in equilibrium. This is where the quantity demanded and quantity supplied are equal. The corresponding price is the equilibrium price or market-clearing price, the quantity is the equilibrium quantity.

Suppose D1 and S1 are the initial market demand curve and the initial market supply curve, respectively. The initial equilibrium is established at point E1, where the market demand curve and the market supply curve intersects each other. Accordingly, the equilibrium price is OP1 and the equilibrium quantity demanded is Oq1.

Now, if there is an increase in the market demand, the market demand curve shifts parallely rightwards to D2 from D1, while the market supply curve remains unchanged at S1. This implies that at the initial price OP1, there exist excess demand equivalent to (Oq'1 - Oq1) units. This excess demand will increase competition among the buyers and they will now be ready to pay a higher price to acquire more units of the good. This will further raise the market price. The price will continue to rise till it reaches OP2. The new equilibrium is established at point E2, where the new demand curve D2 intersects the supply curve S1.

Hence, an increase in demand with supply remaining constant, results in rise in the equilibrium price as well as the equilibrium quantity.

Market of a commodity is in equilibrium. Demand for the commodity 'increases'. Explain the chain of effects of this change till the market again reaches equilibrium. Use diagram.

An increase in the demand for the commodity leads to an increase in the equilibrium price and quantity.

Here,

D1D1 and S1S1 represent the market demand and market supply respectively. The initial equilibrium occurs at E1, where the demand and the supply intersect each other. Due to the increase in the demand for the commodity, the demand curve will shift rightward parallel fromD1D1 to D2D2, while the supply curve will remain unchanged. Hence, there will be a situation of excess demand, equivalent to (q1' − q1). Consequently, the price will rise due to excess demand. The price will continue to rise until it reaches E2 (new equilibrium), where D2D2 intersects the supply curve S1S1. The equilibrium price increases from P1 to P2 and the equilibrium output increases from q1 to q2.

Switch

Switch