Short Answer Type

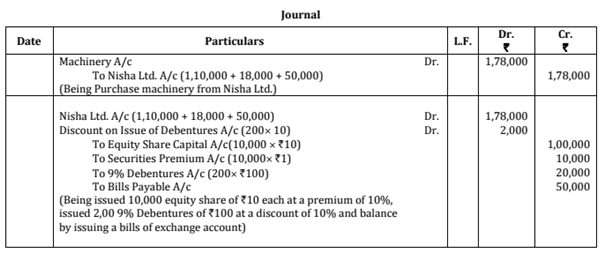

Short Answer TypeDisha Ltd purchased machinery from Nisha Ltd. and paid to Nisha Ltd. as follows :

(i) By issuing 10,000 equity shares of ₹ 10 each at a premium of 10%

(ii) By issuing 200, 9% debentures of ₹ 100 each at a discount of 10%.

(iii) Balance by accepting a bill of exchange of ₹ 50,000 payable after one month.

Pass necessary journal entries in the books of Disha Ltd. for the purchase of machinery and making payment to Nisha Ltd.

BPL Ltd. converted 500, 9% debentures of ₹ 100 each issued at a discount of 6% into equity shares of ₹ 100 each issued at a premium of ₹ 25 per share. Discount on issue of 9% debentures has not yet been written off.

Showing your working notes clearly, pass necessary journal entries for conversion of 9% debentures into equity shares.

State whether the following will increase, decrease or have no effect on cash flow from operating activities while preparing 'Cash Flow Statement':

(i) Decrease in outstanding employees benefits expenses by ₹3,000

(ii) Increase in prepaid insurance by 2,000

Will 'acquisition of machinery by issue of equity shares' be considered while preparing 'Cash Flow Statement? Give reason in support of your answer.

Financial Statements are prepared following the constituent accounting concepts principles procedures and also the legal environment in which the business organisationoperate. These statements are the source of information on the basis of which conclusions are drawn about the profitability and financial position of a

company so that their users can easily understand and use them in their economic decisions in a meaningful way.

From the above statements identify any two values that a company should observe while preparing its financial statements. Also, State under which major headings and sub-headings the following items will be presented in the Balance Sheet of a company as per Schedule III of the Companies Act 2013.

(i) Capital Reserve

(ii) Calls-in-Advance

(iii) Loose Tools

(iv) Bank Overdraft

The proprietary ratio of M Ltd. is 0.80:1 State with reasons whether the following transactions will increase, decrease or not change the proprietary ratio:

(i) Obtained a loan from bank ₹ 2,00,000 payable after five years.

(ii) Purchased machinery for cash ₹ 75,000

(iii) Redeemed 5% redeemable preference shares ₹ 1,00,000

Issued Equity shares to the vendors of machinery purchased for ₹ 4,00,000.

Long Answer Type

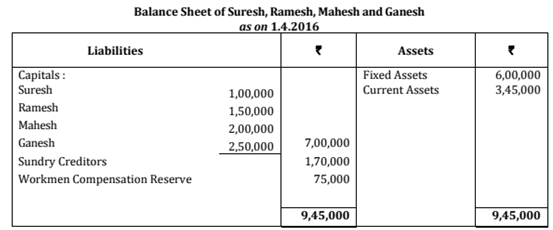

Long Answer TypeSuresh, Ramesh, Mahesh and Ganesh were partners in a firm sharing profits in the ratio of 2:2:3:3. On 1.4.2016 their Balance Sheet was as follows:

From the above date the partners decided to share the future profits equally. For this purpose the goodwill of the firm was valued at ₹ 90,000.

It was also agreed that:

(i) Claim against Workmen Compensation Reserve will be estimated at ₹ 1,00,000 and fixed assets will be depreciated by 10%.

(ii) The capitals of the partners will be adjusted according to the new profit sharing ratio. For this, necessary cash will be brought or paid by the partners as the case may be.

Prepare Revaluation Account, Partners' Capital Accounts and the Balance Sheet of the reconstituted firm.

Pass necessary journal entries on the dissolution of a partnership firm in the following cases:

(i) Expenses of dissolution were ₹ 9,000.

(ii) Expenses of dissolution ₹ 3,400 were paid by a partner, Vishal.

(iii) Shiv, a partner, agreed to do the work for dissolution for a commission of ₹ 4,500. He also agreed to bear the dissolution expenses. Actual dissolution expenses ₹ 3,900 were paid from the firm's bank account.

(iv) Naveen, a partner, agreed to look after the dissolution work for which he was allowed a remuneration of ₹ 3,000. Naveen also agreed to bear the dissolution expenses. Actual expenses on dissolution ₹ 2,700 were paid by Naveen.

(v) Vivek, a partner, was appointed to look after the dissolution work for a remuneration of ₹ 7,000. He agreed to bear the dissolution expenses. Actual dissolution expenses ₹ 6,500 were paid by Rishi, another partner, on behalf of Vivek.

(vi) Gaurav, a partner, was appointed to look after the work of dissolution for a commission of ₹ 12,500. He agreed to bear the dissolution expenses. Gaurav took over furniture of ₹ 12,500 as his commission. The furniture had already been transferred to realisation account.

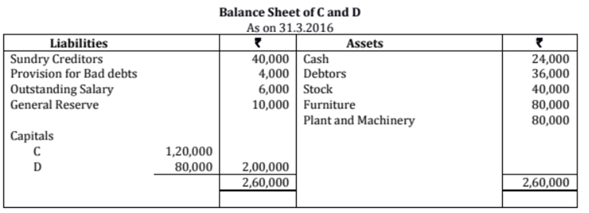

C and D are partner in a firm sharing profits in the ratio of 4:1. On 31.3.2016 their Balance Sheet was as follows:

On the above date, E was admitted 1/4 th share in the profits of the following terms:

(i) E will bring 1,00,000 as his capital and 20,000 for his share of goodwill premium half of which will be withdrawn by C and D.

(ii) Debtors 2,000 will be written off as bad debts and a provision of 4% will be created on debtors for bad debts and doubtful debts.

(iii) Stock will be reduced by ₹2,000, furniture will be depreciated by ₹4,000 and 10% depreciation will be charged on plant and machinery.

(iv) Investments of 7,000 not shown in the Balance Sheet will be taken into account.

(v) There was an outstanding repairs bill of ₹ 2,300 which will be recorded in the books.

Pass necessary Journal entries for the above transactions in the books of the firm on E's admission.

Switch

Switch