Short Answer Type

Short Answer TypeIn the absence of partnership deed the profits of a firm are divided among the partners:

(a) In the ratio of capital

(b) Equally

(c) In the ratio of time devoted for the firm's business

(d) According to the managerial abilities of the partners

(b) Equally: According to partnership act 1932, in the absence of any partnership deed, profits of the firm are divided among the partners equally.

A, B, C and D were partners in a firm sharing profits in the ratio of 4:3:2:1. On 1-1-2015 they admitted E as a new partner for 1:10 share in the profits. E brought Rs 10,000 for his share of goodwill premium which was correctly recorded in the books by the accountant. The accountant showed goodwill at Rs 1,00,000 in the books. Was the accountant correct in doing so? Give reason in support of your answer.

On the retirement of Hari from the firm of 'Hari, Ram and Sharma' the balance-sheet showed a debit balance of Rs 12,000 in the profit and loss account. For calculating the amount payable to Hari this balance will be transferred

(a) to the credit of the capital accounts of Hari, Ram and Sharma equally

(b) to the debit of the capital accounts of Hari, Ram and Sharma equally

(c) to the debit of the capital accounts of Ram and Sharma equally

(d) to the credit of the capital accounts of Ram and Sharma equally

Kumar, Verma and Naresh were partners in a firm sharing profit & loss in the ratio of 3: 2: 2. On 23rd January, 2015 Verma died. Verma's share of profit till the date of his death was calculated at Rs 2,350.

Pass necessary journal entry for the same in the books of the firm.

On 1-4-2013 Jay and Vijay, entered into partnership for supplying laboratory equipment’s to government schools situated in remote and backward areas. They contributed capitals of Rs 80,000 and Rs 50,000 respectively and agreed to share the profits in the ratio 3: 2. The partnership deed provided that interest on capital shall be allowed at 9% per annum. During the year the firm earned a profit of Rs 7,800.

Showing your calculations clearly, prepare 'Profit and Loss Appropriation Account' of Jay and Vijay for the year ended 31-3-2014.

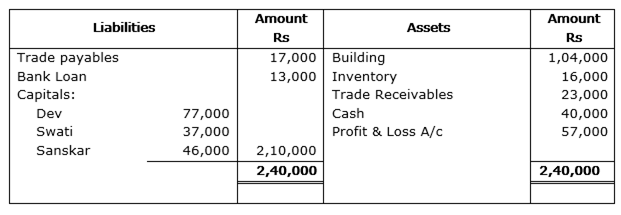

Dev, Swati and Sanskar were partners in a firm sharing profits in the ratio of 2:2:1. On 31-3-2014 their Balance Sheet was as follows:

On 30thJune, 2014 Dev died. According to partnership agreement Dev was entitled to interest on capital at 12% per annum. His share of profit till the date of his death was to be calculated on the basis of the average profits of last four years. The profit of the last four years were:

| Years | Profit (RS) |

| 2010-2011 | 2,04,000 |

| 2011-2012 | 1,80,000 |

| 2012-2013 | 90,000 |

| 2013-2014(Loss) | 57,000 |

On 1-4-2014, Dev withdrew Rs 15,000 to pay for his medical bills.

Prepare Dev's account to be presented to his executors.

Kumar, Gupta and Kavita were partners in a firm sharing profits and losses equally. The firm was engaged in the storage and distribution of canned juice and its godowns were located at three different places in the city. Each godown was being managed individually by Kumar, Gupta and Kavita. Because of increase in business activities at the godown managed by Gupta, he had devote more time. Gupta demanded that his share in the profits of the firm be increased, to which Kumar and Kavita agreed. The new profit sharing ratio was agreed to be 1: 2: 1. For this purpose the goodwill of the firm was valued at two years purchase of the average profits of last five years. The profits of the last five years were as follows:

| Year | Profit (Rs) |

| I | 4,00,000 |

| II | 4,80,000 |

| III | 7,33,000 |

| IV | 33,000 |

| V | 2,20,000 |

You are required to:

(i) Calculate the goodwill of the firm.

(ii) Pass necessary Journal Entry for the treatment of goodwill on change in profit sharing ratio of Kumar, Gupta and Kavita,

On 1-4-2010 Sahil and Charu entered into partnership for sharing profits in the ratio of 4: 3. They admitted Tanu as a new partner on 1-4-2012 for 1/5th share which she acquired equally from Sahil and Charu. Sahil, Charu and Tanu earned profits at a higher rate than the normal rate of return for the year ended 31-3-2013. Therefore, they decided to expand their business. To meet the requirements of additional capital they admitted Puneet as a new partner on 1-4-2013 for 1/7th share in profits which he acquired from Sahil and Charu in 7: 3 ratio.

Calculate:

(i) New profit sharing ratio of Sahil, Charu and Tanu for the year 2012-13.

(ii) New profit sharing ratio of Sahil, Charu, Tanu and Puneet on Puneet's admission.

Joy Ltd. issued 1,00,000 equity shares of Rs 10 each. The amount was payable as follows:

On application Rs 3 per share.

On allotment Rs 4 per share.

On 1st and final call balance.

Applications for 95,000 shares were received and shares were allotted to all the applicants. Sonam to whom 500 shares were allotted failed to pay allotment money and Gautam paid his entire amount due including the amount due on first and final call on the 750 shares allotted to him along with allotment. The amount received on allotment was

(a) Rs 3,80,000

(b) Rs 3,78,000

(c) Rs 3,80,250

(d) Rs 4,00,250

Switch

Switch